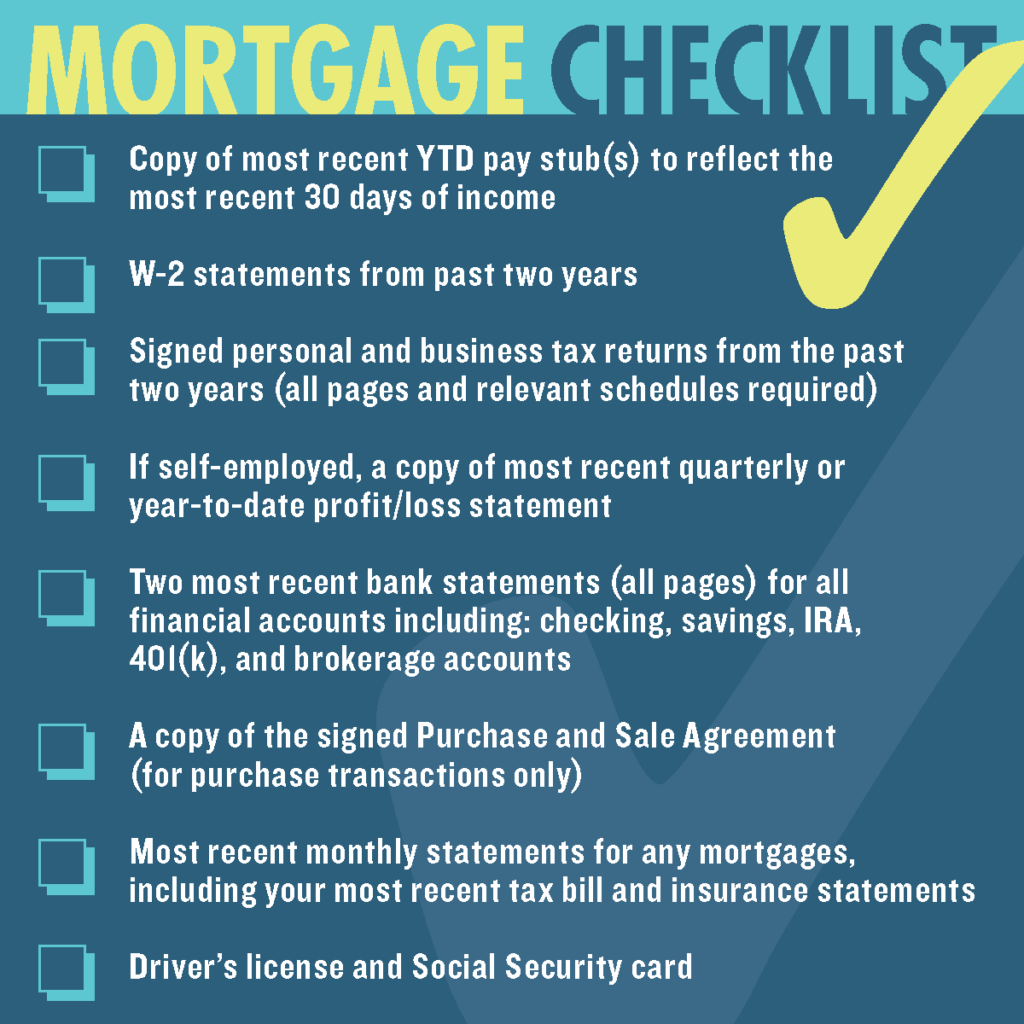

Income

Provide your last two paystubs along with your W2s and Federal tax returns for the last two years (include all schedules). State returns are not needed.

If you are self-employed, ask me for the additional documentation requirements.

If you receive bonus or commissions or have changed your job or position, let’s talk.

Assets

Combine all the funds needed to close into one account at least two months prior to your application.

Document any other deposits here as each could be scrutinized.

Deposits

Deposit checks individually.

Don’t deposit cash without clear proof of the source.

Liquidation

If you are going to sell stocks, bonds, investments or borrow against a retirement account, do it now. Cashing out now may cost you a few dollars in additional gains, but it also protects against losses.

Current Housing

If you own and are selling, provide a copy of your Closing Disclosure.

If you own and are not selling, you’ll need to qualify for both homes or meet the requirements for renting the current.

If you are renting, show 12 months of canceled checks demonstrating timely payments and/or written verification from your management company. Ideally, pay your rent on the same day each month on or prior to its due date.

If you live with family, you may need a letter stating that you live rent-free.

Credit

Check your credit report at www.annualcreditreport.com. Identify any errors now and consult with us for the correct action to take.

If you co-signed a loan or are being reimbursed for a loan that’s in your name, you’ll need at least six months of checks to exclude it.

Avoid new credit or inquiries. These can lower your score and increase your rate.

Employment Stability

Ideally, you’ll have two years or more with your current employer.

Consult with us before changing employers, position or method of compensation. For example, don’t switch from salary to commissions.

|