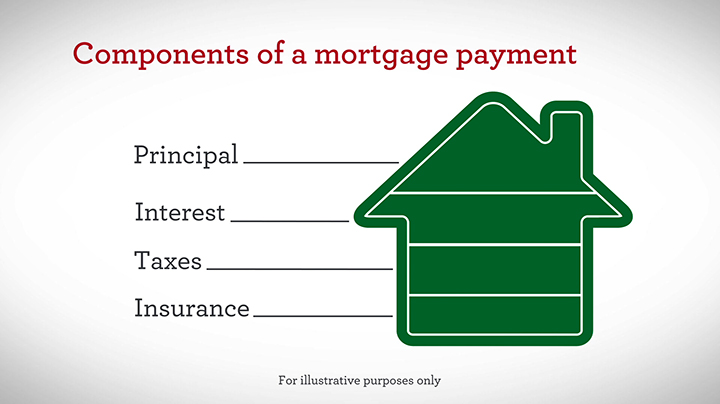

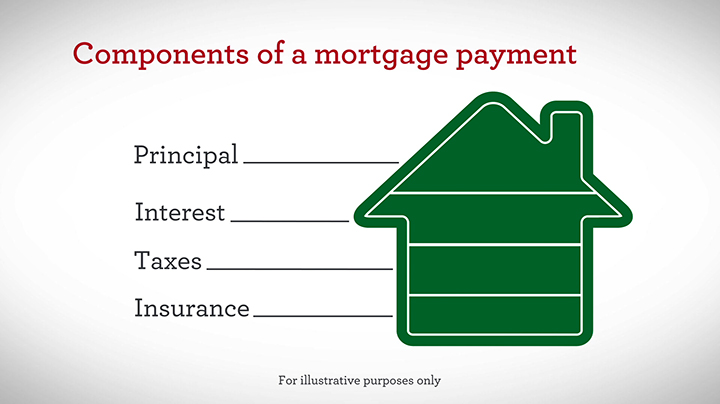

Typical payments consist of four main parts. The acronym PITI is commonly referred to when referring to all the parts of the mortgage.

P – Principal. The principal is the balance of the loan. For easy math go with a $300,000 mortgage has a $300,000 principal. Each month homeowners pay down the principal of their loan.

I – Interest. This is what we hear about on the news so much. Interest rates are what owners pay their lenders/banks/etc. based on percentage each month. So, a lower interest rate means a lower mortgage payment and the same can be said for a higher interest rate.

T – Taxes. Taxes include one or both of either real estate or property taxes. These taxes, like all others, help fund public services. But, some mortgage companies can impound taxes and pay the taxes quarterly or yearly as needed.

I – Insurance. Just like taxes, insurance is paid monthly and is held with escrow until the bill needs to be paid. Every homeowner pays property insurance but only buyers who paid a down payment less than 20% pay PMI additionally. PMI is insurance in the event that the buyer defaults on their loan.

Very rarely do mortgages not include taxes and insurance, but it does happen. Those monthly payments are of course, lower but the homeowner than has to pay a large chunk of money when the tax and insurance bills are due.

How Mortgage Payments Work

Now that you know what goes into each payment, it’s time to start paying off your loan.

When To Pay

Your first mortgage payment will be due after the first full month following your closing date. For example, if you close on June 9, your closing costs will cover the interest you would accrue for the rest of June. After that, your payment for the month of July will be due on August 1.

While monthly mortgage payments are most common, your lender may give you the option to make biweekly payments. With a biweekly payment schedule, your payment becomes more manageable because it’s cut in half. Rocket MortgageⓇ offers monthly and biweekly payments without charging additional fees.

How To Make A Payment

Just as you might go online to make a car insurance or phone bill payment, you can pay your mortgage in the same way. You can still make payments by mail or phone, but the ease and convenience of paying online makes it a more favorable option among most homeowners. One reason for this is the ability to set up automatic payments, either through your bank or directly with your lender.

You should keep in mind that mortgage payments sometimes change. The amount necessary for taxes and insurance may go up or down every year. The same is true if you’re in an adjustable-rate mortgage (ARM) at the end of its fixed period. By setting up an automatic payment through a lender as opposed to the bank, you can make sure the payment isn’t too low and that you’re not overpaying when your escrow or rate goes down.

Making Extra Payments

If you have the means, paying extra toward your principal can potentially save you thousands of dollars in the long run. Whether you pay a little extra every month or make an extra payment throughout the year, the total interest you pay is reduced, and you could potentially pay off your mortgage early. If your main goal is to build equity or save money on interest, paying extra on your mortgage every month might make sense for you.

Before getting started, you should check with your lender to find out if there’s a prepayment penalty for your loan.

Removing PMI

PMI is typically no longer required once the home’s loan-to-value ratio (LTV) is 80% or less. LTV compares how much you borrow with the value of the home you’re borrowing against. It’s calculated as the amount to be borrowed divided by the home’s value and is generally expressed as a percentage. By law, PMI must be removed once the home’s LTV reaches 78% based on the original payment schedule at closing.

Missing Payments

Typically, you won’t have to pay a penalty if you’re only a few days late on your mortgage payment. Most lenders provide a grace period for borrowers to make a late payment without having to pay an additional late fee. Most grace periods are around 15 calendar days, but you should verify this with your lender to be certain of their late payment policy.

It’s important that you contact your lender if you’re going to miss a mortgage payment. Waiting to resolve the issue can lead to defaulting on your loan. Consequences could include late payment fees, penalties and a drop in your credit score, which you’ll then need to repair for future loans.

Falling behind on your payments can also lead to legal action and foreclosure. Your lender can offer you several options designed to help you get back on track with your mortgage payments.